The cost of goods sold,inventory, and gross margin shown in Figure 10.15 were determined from the previously-stated data,particular to perpetual FIFO costing. When applying apply perpetual inventory updating, a second entry made at the same time would record the cost of the item based on LIFO, which would be shifted from merchandise inventory (an asset) to cost of goods sold (an expense). When applying perpetual inventory updating, a second entry made at the same time would record the cost of the item based on FIFO, which would be shifted from merchandise inventory (an asset) to cost of goods sold (an expense).

Calculation for the Ending Inventory Adjustment under Periodic/Specific Identification Methods

- The outcomes for gross margin, under each of these differentcost assumptions, is summarized in Figure 10.21.

- Remember, cost of goods sold is the cost to the seller of the goods sold to customers.

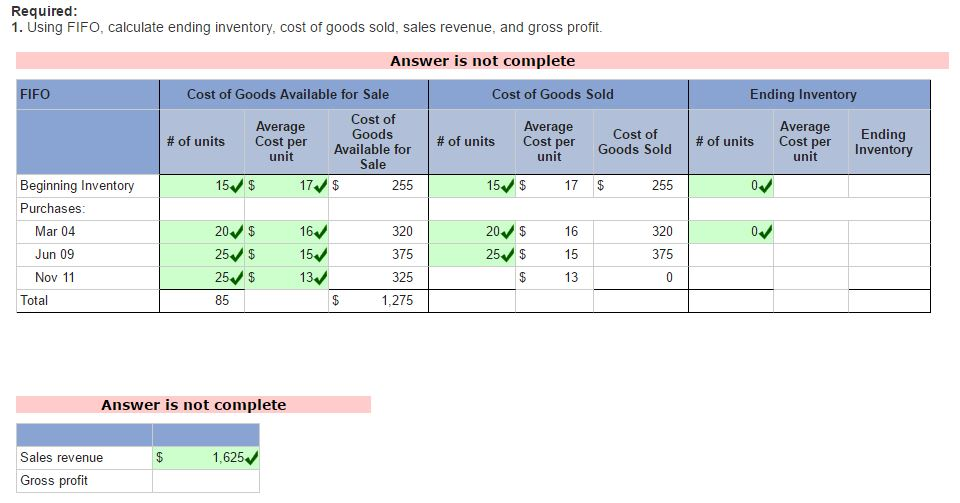

- First in, first out (FIFO) assumes that the oldest items purchased by the company were used in the production of the goods that were sold earliest.

- We will be using the perpetual inventory system in these examples which constantly updates the inventory account balance to reflect inventory on hand.

- The specific identification costing assumption tracks inventory items individually, so that when they are sold, the exact cost of the item is used to offset the revenue from the sale.

They are, therefore, treated as period expenses and reduce the current period’s income. For example, imagine the effort in counting the ending inventory of a large department store. For these reasons, some firms, especially those in the retail sector, use estimation procedures.

Comparison of All Four Methods, Perpetual

Ending inventory is the value of goods still available for sale and held by a company at the end of an accounting period. The dollar amount of ending inventory can be calculated using multiple valuation methods. Although the physical number of units in ending inventory is the same under any method, the dollar value of ending inventory is affected by the inventory valuation method chosen by management. One method for calculating ending inventory is by conducting a physical count of the quantity of each item in inventory.

Understanding Inventory Valuation Methods:

Calculating ending inventory is a crucial task for businesses to accurately assess their financial position and make informed decisions. By understanding the various methods and techniques for calculating ending inventory, you can ensure that your financial statements reflect the true value of your inventory. Whether you opt for the physical count method, use your inventory system quantities, or apply the gross profit method, accurately calculating ending inventory is essential for managing costs, profitability, and tax liabilities. To calculate the cost of goods sold, you need to know the total cost of the items sold during the accounting period. This information can be obtained from sales records, invoices, and other relevant documentation. As you’ve learned, the perpetual inventory system is updatedcontinuously to reflect the current status of inventory on anongoing basis.

Description of Journal Entries for Inventory Sales, Perpetual, Last-in, First-out (LIFO)

The cost ofgoods sold, inventory, and gross margin shown in Figure 10.13 were determined from the previously-stated data,particular to specific identification costing. As you’ve learned, the periodic inventory system is updated at the end of the period to adjust inventory numbers to match the physical count and provide accurate merchandise inventory values for the balance sheet. The adjustment ensures that only the inventory costs that remain on hand are recorded, and the remainder of the goods available for sale are expensed on the income statement as cost of goods sold. Here we will demonstrate the mechanics used to calculate the ending inventory values using the four cost allocation methods and the periodic inventory system. Regardless of which cost assumption is chosen, recordinginventory sales using the perpetual method involves recording boththe revenue and the cost from the transaction for each individualsale. Regardless of which cost assumption is chosen, recording inventory sales using the perpetual method involves recording both the revenue and the cost from the transaction for each individual sale.

These quantities are multiplied by the actual unit costs based on the company’s chosen cost flow assumption, such as FIFO or weighted-average. When it comes to managing your business’s finances, calculating ending inventory is a critical step. Knowing the value of your sellable inventory at the end of how does leasing a car work an accounting period is essential for determining costs, profits, and tax liabilities. Petersen and Knapp allegedly participated in channel stuffing,which is the process of recognizing and recording revenue in acurrent period that actually will be legally earned in one or morefuture fiscal periods.

Cost of goods sold was calculated to be $9,360, which should be recorded as an expense. The inventory at period end should be $8,955, requiring an entry to increase merchandise inventory by $5,895. Cost of goods sold was calculated to be $7,200, which should be recorded as an expense. For The Spy Who Loves You, considering the entire period, 300 of the 585 units available for the period were sold, and if the earliest acquisitions are considered sold first, then the units that remain under FIFO are those that were purchased last. Following that logic, ending inventory included 210 units purchased at $33 and 75 units purchased at $27 each, for a total FIFO periodic ending inventory value of $8,955. Subtracting this ending inventory from the $16,155 total of goods available for sale leaves $7,200 in cost of goods sold this period.

Journal entries are not shown, but the following discussion provides the information that would be used in recording the necessary journal entries. Each time a product is sold, a revenue entry would be made to record the sales revenue and the corresponding accounts receivable or cash from the sale. The cost of goods sold, inventory, andgross margin shown in Figure 10.19 were determined from the previously-stated data,particular to perpetual, AVG costing.

It has grown since the 1970s alongside the development of affordable personal computers. These UPC codes identify specific products but are not specific to the particular batch of goods that were produced. Electronic product codes (EPCs) such as radio frequency identifiers (RFIDs) are essentially an evolved version of UPCs in which a chip/identifier is embedded in the EPC code that matches the goods to the actual batch of product that was produced. This more specific information allows better control, greater accountability, increased efficiency, and overall quality monitoring of goods in inventory. The technology advancements that are available for perpetual inventory systems make it nearly impossible for businesses to choose periodic inventory and forego the competitive advantages that the technology offers.

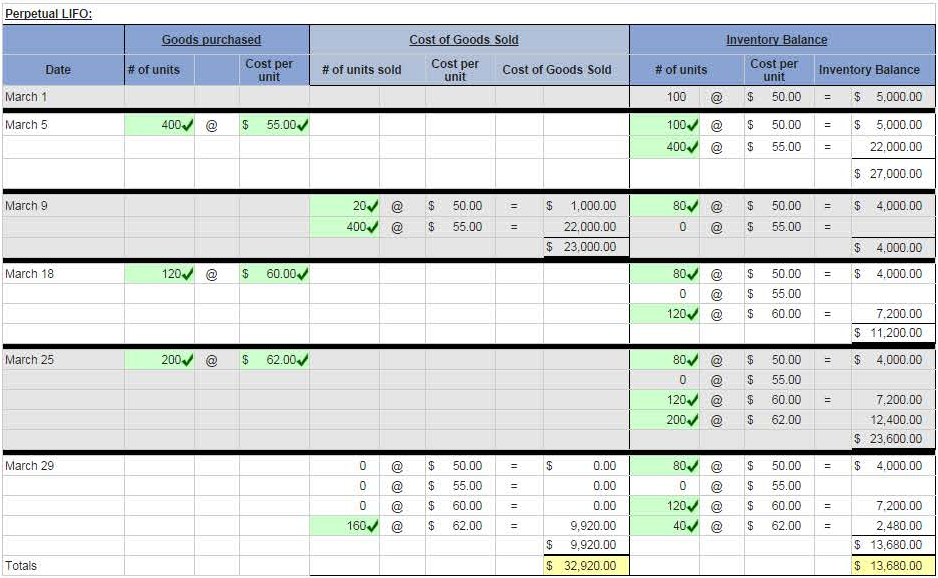

The last-in, first-out method (LIFO) of cost allocation assumesthat the last units purchased are the first units sold. At the time of the second sale of 180 units, the LIFOassumption directs the company to cost out the 180 units from thelatest purchased units, which had cost $27 for a total cost on thesecond sale of $4,860. Thus, after two sales, there remained 30units of beginning inventory that had cost the company $21 each,plus 45 units of the goods purchased for $27 each. Ending inventory was made up of 30 units at $21 each, 45units at $27 each, and 210 units at $33 each, for a total LIFOperpetual ending inventory value of $8,775.